|

The numbers are in for the first three quarters of 2017: overall deal volume and value are up in the US middle market.

-

“Middle-market PE funds are on track for another stellar year of fundraising... ” 1

Pitchbook

-

“About 68 percent of executives at US-headquartered corporations and 76 percent of leaders at domestic-based private equity firms say deal flow will increase in the next 12 months. Further, most respondents believe deal size will either increase (63 percent) or stay the same (34 percent), compared with deals brokered in 2017. ” 2

Deloitte

Analysts attribute a significant portion of these gains to: a spike in activity in the upper-middle-market, PE firms preferring larger deals, increasing valuations and funds’ success raising capital for investment.

So, What’s Happening In The Lower-Middle-Market?

The question for you—a successful owner of a lower-middle-market company is—What do these trends mean to you? Is 2018 the year to sell or find an investor for your company?

Which kinds of companies are selling? Or put another way, what are buyers looking for?

Let’s turn again to the experts:

-

“From a sector perspective, technology and healthcare will drive M&A activity in North America because of the US’s strength in tech innovation and the aging populations in advanced economies. Further consolidation within the energy and raw materials sectors should also continue to generate transactions in the coming years.” 3

Baker McKenzie / Oxford Economics

-

“Lower-middle-market companies are often ideal targets for buy and build strategies which have experienced a groundswell of popularity as PE firms focus more on operational improvements...”.4

Pitchbook

-

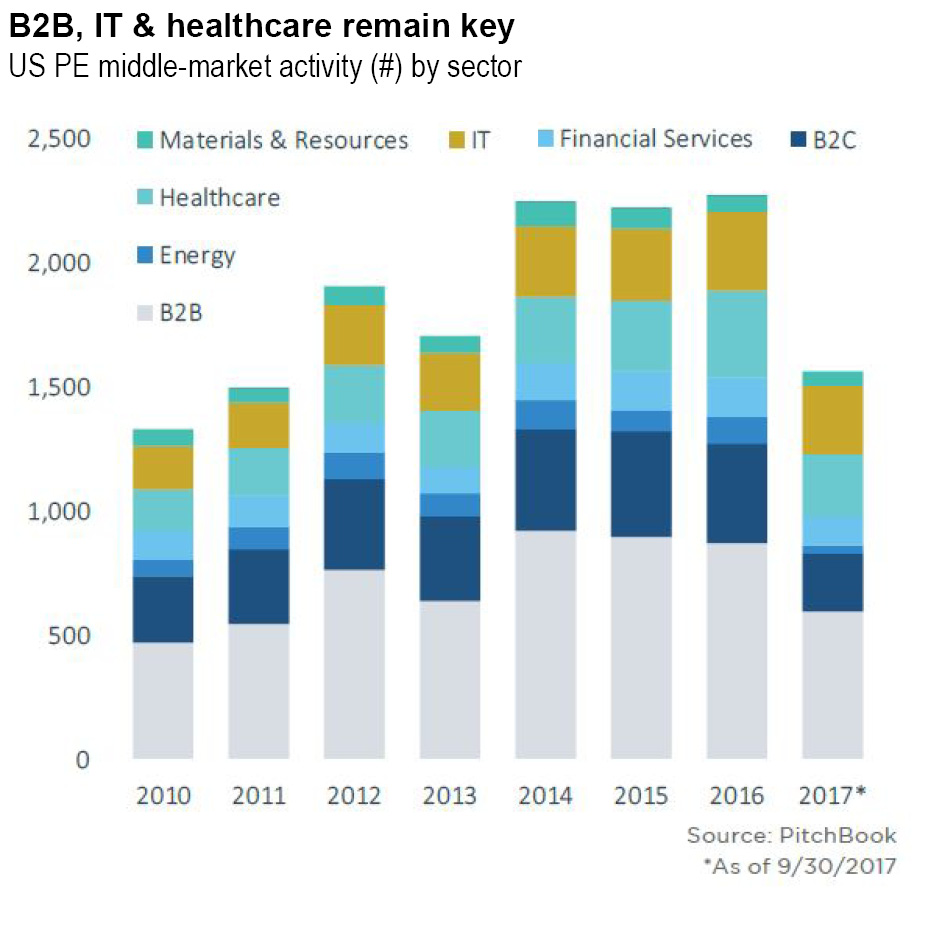

In terms of activity by sector, IT, B2B and healthcare remain strong, with IT companies bolstering deal value.

5

-

Private equity activity is increasing in the restaurant and bar sector (especially mid-market restaurant and fast casual) for the first time since 2005.

Do You Sell or Do You Stay?

None of the experts have a crystal ball and we don’t either. But we do have a data-driven process to help you determine if 2018 is the right time to put your business on the market.

Our Proactive Sale Strategy™ assesses your company’s marketplace and its sale readiness. It realistically estimates your company’s value and likely sale price. We are experts in identifying a company’s competitive advantage and the active buyers in the marketplace looking to acquire that advantage.

Kevin Short is the author of Sell Your Business For An Outrageous Price and the Managing Partner and CEO of Clayton Capital Partners, a St. Louis-based investment banking firm specializing in the sale and purchase of mid-size companies.

-

Pitchbook limits “middle-market” to US companies acquired for prices between $25M and $1B.

-

Deloitte, The state of the deal: M&A trends 2018, page 1.

-

Baker McKenzie / Oxford Economics, 2017 Global Transaction Forecast, page 16.

-

Pitchbook, p. 7.

-

Pitchbook, p. 7.

|