|

|

|||

|

Issue 19

|

||||

|

VESTING: Handcuffing Key Employees To Your Company In the previous issue of The Exit Planning Navigator®, we outlined the four characteristics of a successful Employee Incentive Plan. Namely, such plans should:

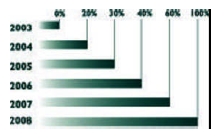

In this issue we focus on the last characteristic; handcuffing the key employees to the business. The goal of the handcuff is to keep the employee with the company the day after, and even years after, the bonus is awarded. To achieve this goal, owners and their advisors typically incorporate several techniques into a stock purchase or nonqualified deferred compensation plan. Vesting Schedule First, a vesting schedule handcuffs employees to the company for a time period necessary to become entitled to the bonus awarded. We prefer a continual or rolling vesting schedule in which a single vesting schedule is applied separately to each year's contribution. Using this schedule, an employee is handcuffed to the company for a long period of time because the key employee is never fully vested in the most recent contribution. Let's assume that a $30,000 award is assigned to an employee: one-half of which is given immediately and the other half subject to a five-year vesting schedule. If the award is earned in 2003, the effect of vesting is demonstrated in the following graph:

As you can see, only in the year 2008 is the employee fully vested in the award earned in 2003. Should the employee leave the company prior to that time, he is only entitled to a percentage of the total award amount. Your key employees are thus "handcuffed" to your business because they receive the full award only by staying with your business. Further, the longer they stay, the more they receive.

Vesting truly handcuffs key people - financially - to your business. Forfeiture Provisions and Payment Schedules Another technique owners use to motivate an employee to stay with the company is forfeiture. A forfeiture provision can be used to reclaim some or all of an employee's vested benefits if he leaves your business and violates his employment agreement. This is an added incentive for your employee to honor any covenant not to compete or trade secret provision contained in his employment agreement. Owners use payment schedules to determine when payments of vested amounts commence and how long they are to be continued after an employee leaves. When payment schedules are combined with forfeiture considerations, they can prevent recently departed employees from using funds from the deferred compensation plan to compete with the former employer. Funding Devices Handcuffing your key employees to your company cannot be effective unless the money to pay the deferred bonus is available when needed. Your key employees must be confident that funding is in place to cover the deferred award. For that reason, owners should seek experienced investment and tax advice. The choice of funding vehicles can influence the timing and amount of income taxes at the company level. Check with your professional advisors to see how these handcuffing techniques can become part of the design of your employee incentive plan. Remember, a successful bonus plan for your employees ultimately bodes well for the success of your own Exit Plan. Subsequent issues of The Exit Planning Navigator® discuss all aspects of Exit Planning.

|

||||

|

||||

|

||||